As the world undertakes an energy transition towards a more environmentally friendly global energy balance, the future of natural gas is at a crossroads. It may be doomed to decline like coal and oil, or take their place because it emits fewer greenhouse gases (GHGs). But what is natural gas? How was it formed? From extraction to end use, what is its chain of production?

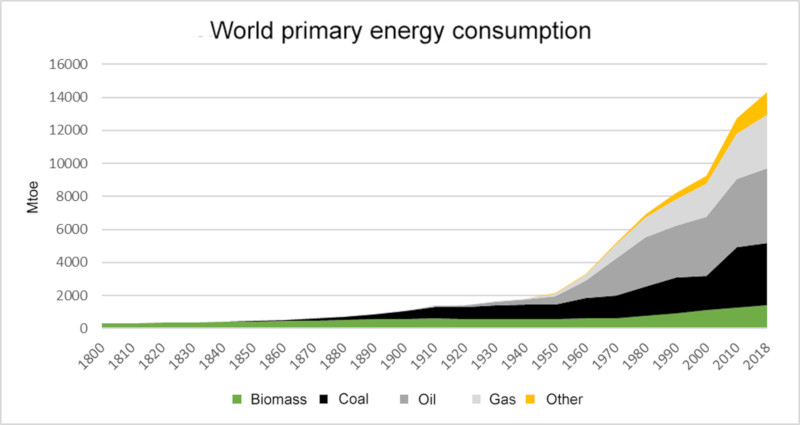

Like coal in the 19th century and oil in the 20th century, is natural gas becoming the fossil fuel of the 21st century? The growth in its consumption and the evolution of its place in the world energy balance point in this direction (Image 1). While it accounted for only 7% of world primary energy consumption in 1950 (153 million tons of oil equivalent (Mtoe)), it reached 16% in 1980 (1,158 Mtoe), 21% in 2000 (2,026 Mtoe[1]) and finally 23% (3,260 Mtoe) in 2018[2].

This boom is linked to the growth of the world population, which rose from 2.5 billion inhabitants in 1950 to 7.6 billion at the beginning of 2019, and will no doubt go on to reach 9 to 10 billion by 2050. It is also tied to economic growth, which is currently moderate in developed countries, but strong in emerging countries such as China and India, which are determined to catch up. However, this boom is also due to the specific characteristics of natural gas, its techniques and its industry.

Image 1: Primary energy consumption by source between 1800 and 2018. [Source: BP Statistical Review]

1. What is natural gas?

Like all hydrocarbons, natural gas is composed of carbon (C) and hydrogen (H) atoms, but at normal temperature and pressure, compounds of these atoms are in gaseous form. Natural gas is made up mainly of methane (CH4), but also propane (C3H8), butane (C4H10), ethane (C2H6) and pentane (C5H12). The proportions of these different types of gas vary from one deposit to another, but methane is always dominant, ranging from 70 to 98% of the molecular weight.

Because of these differences, not all gases have the same calorific value[3] (Read: Les unités énergétiques, Energy Units). In France for example, the gas consumed in the North, coming from the Netherlands and called L-gas (known in France as gaz B), has a high nitrogen content and a low-calorific value, hence an equivalence of less than 10 kWh/m3, whereas the gas coming from Norway, Russia or Algeria, known as H-gas (gaz A in France), is closer to 12 kWh/m3.

2. Exploration and production

Video: Natural gas basic information. [Source: Student Energy]

Originally, gas was long considered a dangerous and troublesome by-product in oil wells (Read: Gaz naturel : une histoire très ancienne, Natural Gas: a very old story). It was flared on site. Then in the 19th century, the first gas fields were drilled, but uses remained limited, but it was only after the construction of several thousand kilometers of gas pipelines in the United States that gas uses, first industrial and then domestic, developed. (Read: L’essor du gaz naturel au 20ème siècle partie 1 et partie 2, The Rise of Natural Gas in the 20th Century).

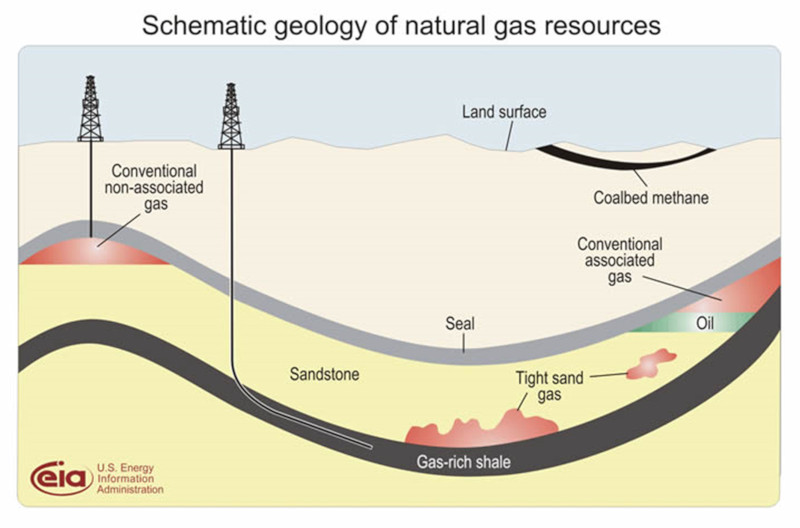

Conventional gas trapped in the subsoil is easily accessible. It is concentrated in the pores of underground rocks and naturally trapped under pressure, under a layer of impermeable rock that isolates it in a reservoir (Image 2). Gas may be associated or non-associated. In the case of the former, the gas is dissolved in crude oil and must be separated when the oil is extracted. Formerly considered as waste, such gas is now either re-injected into the oil reservoir to maintain pressure or is recovered. Non-associated gas may be present in oil deposits but not mixed with the oil (Read: Géologie et géodynamique des hydrocarbures, Hydrocarbon Geology and Geodynamics).

Image 2: Natural gas in the subsoil. [Source: US Energy Information Administration, http://www.eia.doe.gov/oil_gas/natural_gas/special/ngresources/ngresources.html]

Unconventional gas, which includes shale gas, coalbed methane, tight gas, and methane hydrates, is difficult to extract compared to conventional gas. Historically, gas producers have favored conventional gas, which guarantees a resource recovery rate of 80 % compared to an average of 20 % for unconventional gas[4]. However, the share of the latter has increased sharply in recent years, particularly in the United States (Read: Le pétrole de schistes : formation et extraction, Shale Oil: Formation and Extraction, and La formation du gaz de schistes et son extraction, Shale Gas Formation and Extraction).

Exploration is the search for gas deposits using mapping and seismic techniques. Using a controlled source of seismic energy, artificial shock waves are sent through the earth. Special sensors are used to record the resulting data, which provide information on the geological properties present in the subsurface. From these data, subsurface maps are then drawn up to better evaluate the prospect. If it meets certain selection criteria, an exploration well is drilled in order to confirm the presence of a technically exploitable deposit and to determine its economic potential, i.e. the recoverable reserves, classified as possible, probable, and proved, according to their estimated recovery costs.

In 2020, these reserves are estimated at between 150 and 200 000 billion cubic meters (bcm), distributed across roughly 100 countries including Russia (18%), Iran (17%) and Qatar (13%). They currently represent some fifty years of world consumption, but the estimates are always evolving due to ongoing prospecting in new territories (like the Arctic) and technological advances. The United States, for example, has overtaken Saudi Arabia in proved natural gas reserves as a result of its intense development of shale gas extraction methods and increased exploration efforts. The main players in this activity are the major oil companies such as BP, Chevron, Exxon, Shell, Total and, of course, those in the gas sector such as Gazprom or Engie, which devote a large share of their investments to it.

After the exploration phase, gas extraction requires complex infrastructure, but once the field is drilled, conventional gas, which is naturally under pressure, rises easily to the surface for collection. It is then processed and purified to remove sulphur compounds and CO2 before being put on the market. The United States and Russia are the largest producers, accounting for 20% and 17% of world production respectively. The United States’ share is growing with its strong development of unconventional gas extraction. Next are the Gulf States (Iran, Qatar, and Saudi Arabia in particular), followed by historical producers such as Canada, Norway, Australia, and Algeria.

3. Transport

Gas is most often transported by pipeline from its point of extraction to its storage and/or distribution sites, but it is also transported with increasing frequency in liquefied form for some part of its journey (Read: Les marchés du gaz naturel et du gaz naturel liquéfié – GNL , The natural gas and liquefied natural gas (LNG) markets).

3.1. Pipeline transport

Although the first gas pipeline in the United States began operating in 1891, it was not until the 1960s that metallurgical techniques made it possible to build efficient gas pipelines, and it was not until the 1970s that they stretched for thousands of kilometers. Today, the pipeline network is extremely dense. Worldwide, gas flows through more than a million kilometers of pipelines. In France, they extend over 32,000 km.

Onshore and submarine pipelines carry gas between production sites and points of consumption. Compressor stations are positioned along the network to control gas pressure and recompress the gas; this allows the gas to flow at high speed, but requires added energy consumption.

Image 3: Gas pipeline. [Source: https://viteos.ch]

The Russian giant Gazprom is the largest production and network management company in the world, with the largest transport network (Read: L’industrie du gaz en Russie, The gas industry in Russia). In Europe, many operators, such as the Italian group ENI or GRTgaz in France, transport gas and participate in the development of the transmission system. Engie, a French multinational electric utility, has a large network of pipelines and numerous LNG terminals. Coordinated by the European Union, European operators are developing the interconnection of their networks. Generally speaking, the majority of contracts between an operator (GDF Suez) and a producer (Gazprom) are long-term contracts, which makes it possible to guarantee the profitability of a pipeline while establishing a relationship of trust between the producer and the region where the gas is being received[5].

3.2. Liquefied natural gas transport

When transport by pipeline is too expensive or physically impossible, such as when crossing an ocean, gas is transported in liquid form by dedicated ships called LNG carriers (Image 4).

Image 4: GDF SUEZ Global Energy LNG carrier. [Source: https://www.flickr.com/photos/etienne_valois/6845298863]

At around -161°C, gas can be transported in liquid form, hence the name liquefied natural gas (LNG). This method is an alternative to pipelines, which are permanent, immovable transport infrastructures. LNG reduces the volume of gas by up to 600 times and thus facilitates its transport over long distances. LNG offers more flexibility, as it can be transported by ship from liquefaction plants to regasification terminals to supply areas far from production sites (Image 5). Since the early 2000s, improvements in liquefaction technology and innovations in shipbuilding have led to the growth of LNG, particularly by making long-distance transport more cost-effective.

Image 5: LNG terminal in Dunkirk, France. [Source: ©Dunkerque LNG]

With its four regasification centers (Dunkirk, Montoir de Bretagne, and two in Fos-sur-Mer), France has the third largest reception capacity in Europe. The LNG it consumes comes mainly from Algeria (38% of imported volumes) and Nigeria (30.6%)[6].

4. Storage

In order to be stored in large quantities, natural gas is injected into underground reservoirs of three types: porous rocks that are naturally waterlogged called aquifer reservoirs, caverns dug in layers of salt called salt caverns, and old gas fields that have been shut down called depleted gas reservoirs. In all of these forms of underground storage, the gas is injected under pressure (between 40 and 270 bars), which in turn facilitates its withdrawal. World underground storage capacities were estimated at nearly 360 billion cubic meters in 2014[7], of which ¾ is made up of depleted gas reservoirs.

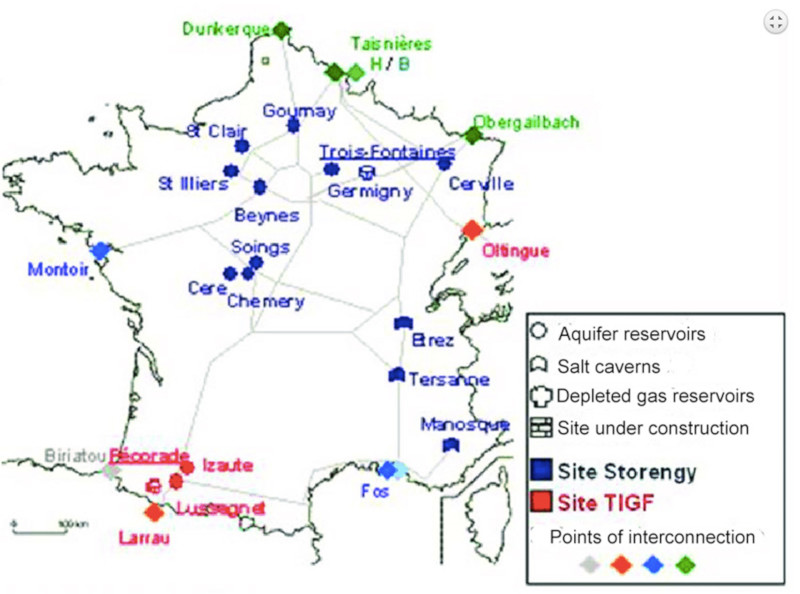

Storage sites enable gas production companies to meet their delivery targets and gas suppliers to manage the utilization rate of the transmission and distribution network while efficiently meeting demand. Russia’s Gazprom and Engie’s subsidiary Storengy have the world’s largest underground storage capacities. In France, these storage facilities are spread throughout the country (Image 6).

Image 6: Underground natural gas storage in France. [Source: https://www.researchgate.net/figure/Carte-des-sites-de-stockage-souterrains-de-gaz-naturel-en-France_fig29_330485577]

Storage facilities play a strategic role because they make it possible to compensate for technical or political problems on the part of suppliers, and to balance supply, which is relatively constant throughout the year, with demand, which varies greatly according to the seasons. These underground reservoirs are filled in the summer, when gas consumption is lower, to provide for periods of high consumption in the winter[8][9]. In accordance with the 2003 European legislation on the liberalization of the gas market, storage capacity held by an operator must be made available to all suppliers in the market.

5. National transmission and distribution

Image 7: The natural gas transmission network in France. [Source: https://www.cre.fr/Gaz-naturel/Reseaux-de-gaz-naturel/Presentation-des-reseaux-de-gaz-naturel]

In each national territory, gas is transported through a national transmission network. In France (Image 7), this network is made up of:

- a network of large-diameter, high-pressure pipelines linking points of interconnection with neighboring networks (Belgium, Germany, Switzerland or Spain), underground storage facilities, LNG terminals, and regional networks; the gas flows through steel pipelines at a speed of around 30 km per hour; to compensate for the drop in pressure caused by friction, compressor stations (between 65 and 95 bars) are installed approximately every 150 km;

- regional networks that extend the main network to large industrial consumers and distribution networks.

These transmission networks are managed by GRTgaz, a subsidiary of Engie, for the low-calorific L-gas network in the North and most of the high-calorific H-gas network, and by TIGF, a subsidiary of a consortium (SNAM, C31, Predica) for the H-gas network in the South-West.

The distribution networks transport the gas at low pressure to final consumers such as households, services, or small industrial companies. In France, they are placed under the responsibility of 25 operators of very different sizes:

- Gaz Réseau Distribution France (GRDF), a subsidiary of Engie, distributes 96% of the market;

- the other 24 distributors, also known as local distribution companies (LDCs), generally operate within the limits of a large city, such as Régaz in Bordeaux, Gaz de Strasbourg (GDS), or Gaz Électricité de Grenoble (GEG).

6. Uses

Natural gas, in the form of methane, is a fuel that is used for many purposes: electricity generation, industrial and domestic heating, powering industrial processes, or motorized transportation.

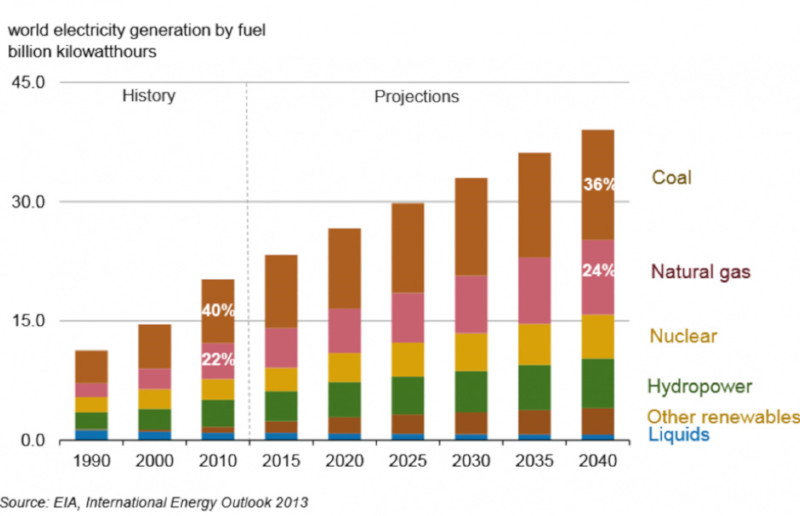

Image 8: Evolution of the world electricity mix by fuel source. [Source: Planète Energies]

Gas provides about a quarter of the world’s electricity (Image 8). This share will only increase as thermal power plants are replaced in the fight against global warming and local air pollution, because the combustion of gas, compared to that of fuel oil or coal, produces fewer particles and fewer greenhouse gases (GHG). Gas can also play a back-up role in electricity production, helping to secure the electricity supply in the face of the increasing use of intermittent and unpredictable renewable sources (Read: La percée du stockage électrique, The breakthrough of electricity storage).

Gas is used in conventional thermal power plants, as well as in so-called Combined Cycle Gas Turbine plants (CCGTs) which combine two types of turbine: a combustion turbine and a steam turbine, connected to an alternator[10]. They operate as follows:

- air taken from the atmosphere is highly compressed in order to increase its pressure and temperature,

- introduced into the combustion chamber, this air is mixed with gas at over 1,000° C,

- the energy generated turns a combustion turbine which drives an alternator producing electricity, while the heat from the exhaust gases is converted into steam,

- this steam is then used to turn a steam turbine that drives its own electricity-producing alternator.

This type of power plant achieves an efficiency of 65% compared to 38% on average in conventional power plants.

Gas is also used to heat residential and tertiary sector buildings, as well as industrial furnaces and boilers. It is also a raw material for chemistry, used, for example, to produce hydrogen and ammonia.

More recently, it has begun to be used in transport for Natural Gas Vehicles (NGV) generally stored under pressure (200 bars) in specific tanks inside the vehicle (Read: L’automobile du futur : quelle source d’énergie ?, The car of the future: which energy source?).

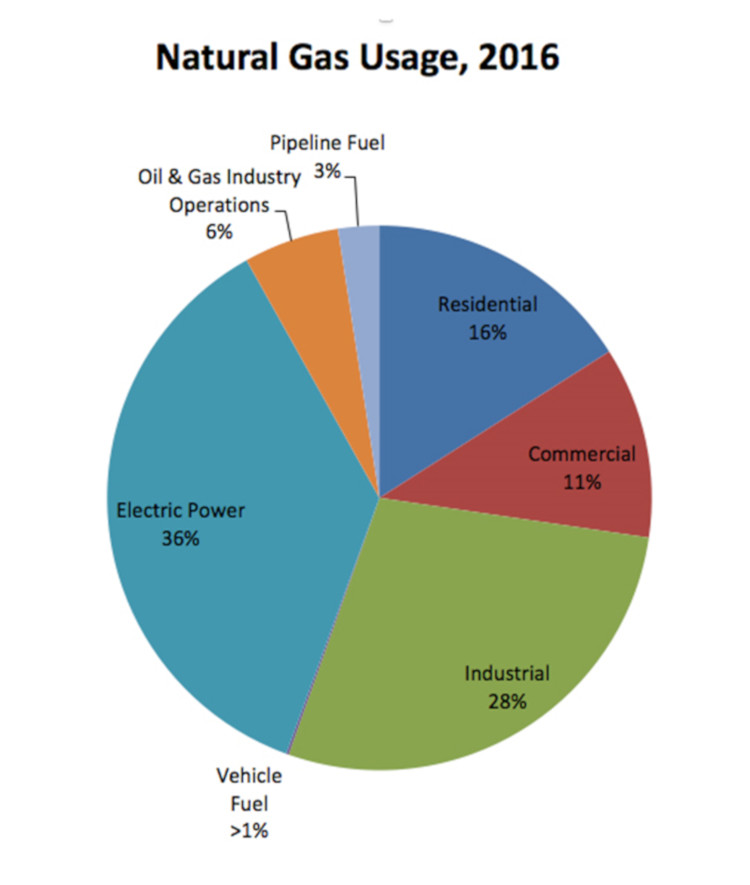

As each country has its own gas consumption patterns, it is difficult to generalize about the structure of these patterns. Some countries, such as Italy, China, Iran and India, have already developed gas mobility to a great extent, while others, such as the United States, are mainly focused on electricity production (Image 9). More than a third of the gas consumed goes to power generation. More than a quarter of the gas consumed is used for industry, with the remainder going to residential heating and the tertiary sector.

Image 9: US natural gas consumption by sector in 2016. [Source: U.S. Energy Information Administration]

7. Environmental Impacts

The advantages of natural gas are well known:

- its combustion emits less CO2 and less fine particles, dust, and sulphur oxides, sources of local pollution;

- its extensive transmission and distribution network eliminates the need for consumers to store the energy they need;

- the growing LNG industry feeds the national grids through maritime transport and LNG terminals, thus increasing security of supply;

- gas is no more expensive than oil for meeting comparable needs.

For all these reasons, gas seems to be the perfect transitional energy to replace the high-carbon fuels coal and oil, which we want to stop using as quickly as possible to limit climate degradation. Moreover, it favors the creation of a less carbon-based energy sector by supporting the development of renewable energies, which require substantial investments and lead times.

In the face of these advantages, certain disadvantages should not be underestimated:

- the infrastructure required for the exploitation and processing of gas fields is particularly energy-intensive, as is transportation, which generates significant GHG emissions through methane leaks on pipelines and losses in the volumes transported in LNG;

- the extraction of unconventional gas is accused of causing landscape deterioration through the increase of drilling heads and heavy pollution of the subsoil and groundwater with chemicals; in addition, hydraulic fracturing is a major water consumer;

- as a source of carbonaceous energy, the combustion of gas emits about 480g/CO2 per kWh of energy produced, making its consumption responsible for one fifth of global CO2 emissions;

- finally, although discoveries of coalbed gas, shale gas, tight gas and methane hydrates have increased the world’s gas reserves, they are more expensive, more energy-intensive and more carbon-intensive to use due to the methods and resources used to extract, transport and use unconventional gas[11].

Thus, we must explore ways to make the gas sector more environmentally friendly:

- if we want to continue to burn natural gas while limiting GHG emissions, we can use carbon capture and storage (CCS) at the exit of thermoelectric power plants or large industrial installations (Read: Captage et stockage du carbone, Carbon capture and storage) ;

- we can also favor the use of biogas, resulting from the fermentation of organic matter (Read: Biomass and Energy);

- in addition, we should make room for new gas production methods that are beginning to emerge: green or renewable gases can be produced from biomass using methanisation and gasification processes, or from green electricity using electrolysis and methanation in a process called “power-to-gas” (P2G). The potential of these sectors is considerable, estimated for France, for example, to be able to satisfy the totality of its gas consumption[12]. In 2019, renewable gas injection facilities are the subject of ambitious political objectives: 10% renewable gas in the French networks by 2030, according to the Energy Transition Law for Green Growth (LTECV) of 2015. Development in this direction will build on the 714 GWh of renewable gas produced and injected into the French gas grid in 2018 via 76 dedicated facilities, an increase of 76% compared to 2017[13]. However, incentives and research and development are still needed to establish a full-fledged green gas production sector!

Notes and references

The Energy Encyclopedia is published by the Association des Encyclopédies de l’Environnement et de l’Énergie (www.a3e.fr), contractually linked to the University of Grenoble Alpes and Grenoble INP, and sponsored by the French Academy of Sciences.

To cite this article, please mention the name of the author, the title of the article and its URL on the Energy Encyclopedia website.

The Energy Encyclopedia articles are made available under the terms of the Creative Commons Attribution-Noncommercial-No Derivative Works 4.0 International License.

[1] https://www.encyclopedie-energie.org/consommation-mondiale-denergie-1800-2000-les-resultats/

[2] BP Statistical Review 2018

[3] In the rest of the text, for simplicity we will use a 10-thermal gas (1,000 kcal)/m3, i.e. 106 m3 =10 GWh.

[4] Favennec Jean-Pierre. Recherche et production du pétrole et du gaz. Réserves, couts et contrats, Ed. Technip.

[5] Connaissance des énergies, https://www.connaissancedesenergies.org/fiche-pedagogique/transport-du-gaz

[6] Selectra, https://selectra.info/energie/guides/comprendre/gaz/production

[7] International Gas Union

[8] Connaissance des énergies, https://www.connaissancedesenergies.org/fiche-pedagogique/stockage-du-gaz

[9] Engie, https://www.engie.com/en/activities/infrastructures/storage

[10] https://www.edf.fr/groupe-edf/espaces-dedies/l-energie-de-a-a-z/tout-sur-l-energie/produire-de-l-electricite/les-differents-types-de-centrales-thermiques

[11] Jancovici J.M., https://jancovici.com/transition-energetique/gaz/quest-ce-que-le-gaz-non-conventionnel/

[12] ADEME, Mix de gaz 100 % renouvelable en 2050 ?

[13] GRDF, Panorama du gaz renouvelable 2018